The End of Correspondent Bank Fees: How to Ensure Your Supplier Receives 100%

By Linka Finance

You approved a $50,000 wire transfer. Your supplier received $49,200. Your bank charged you $40 in sending fees. Where did the other $760 go?

It went to correspondent banks institutions you never hired, never agreed to pay, and whose names never appeared in your contract.

This is one of the most persistent cost leaks in B2B international payments. And for companies in Latin America making regular payments to international suppliers, it quietly inflates the real cost of every transaction.

What Is a Correspondent Bank and Why Does It Cost You Money?

When your bank sends a wire transfer internationally, it rarely has a direct relationship with the recipient's bank. So the payment travels through a chain of one, two, or sometimes three intermediary institutions each one a correspondent bank.

Every bank in that chain is allowed to deduct a handling fee directly from the transfer amount. These fees are not disclosed upfront. Each intermediary along the chain can collect its own charge sometimes without informing either party beforehand typically ranging from $10 to over $100 per hop.

The result: the amount that leaves your account and the amount your supplier receives are two different numbers. And that gap is not predictable.

Why LATAM Corridors Are Hit Harder

Latin America's banking infrastructure is fragmented. Direct relationships between local banks and counterparts in Asia, the U.S., or Europe are limited which means more correspondent hops per payment, and more deduction points.

A 2025 Mastercard/PCMI study found that correspondent banking fees represent 40%–60% of total cross-border transaction costs for SMEs in Latin America, making them the single largest cost driver in the chain.

For a treasurer managing 20 monthly payments to international suppliers, this isn't a minor variance. It's a structural cost that sits entirely outside your negotiated payment terms.

The Hidden Operational Cost: Reconciliation Breaks

The correspondent bank problem creates a second issue that finance teams rarely anticipate: reconciliation gaps.

Your system records the full transfer amount. Your supplier's system records what they actually received. The two numbers don't match triggering supplier disputes, top-up transfer requests, and audit discrepancies.

For companies making 15–30 international payments per month, this noise is a recurring cost in finance team hours. And it's largely invisible on any single report.

Regulators in multiple jurisdictions noted in 2025 that intermediary bank fees are often not disclosed before a transfer is sent meaning your bank may not be able to tell you exactly what your supplier will receive until the payment is already in motion.

How Linka Solves This

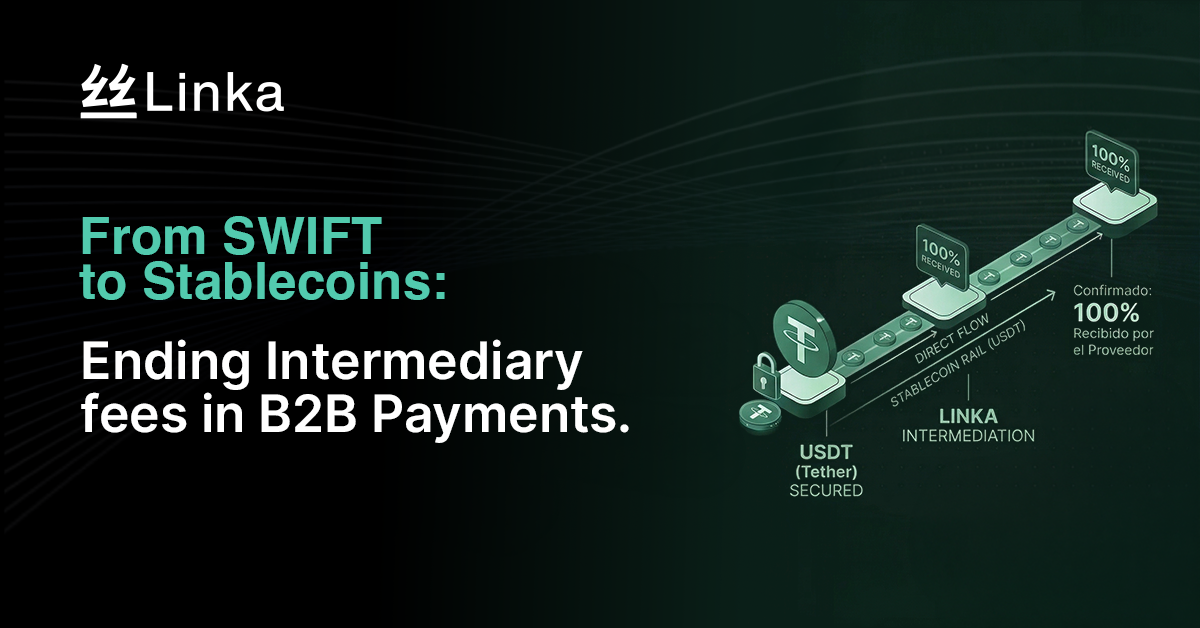

Linka processes international B2B payments across Latin America using stablecoin infrastructure USDT instead of SWIFT correspondent rails.

When a payment moves on-chain, it bypasses the correspondent banking chain entirely. No mid-transfer deductions. The amount sent reaches the conversion point intact.

What the cost structure looks like:

- A single, transparent commission agreed before the transfer moves, no surprises after the fact

- Settlement in under 24 hours for most corridors

- No correspondent bank deductions on the transfer amount

- No SWIFT fees, no OUR/SHA/BEN ambiguity

- No need to hold foreign currency accounts

We're Here to Help

If your team is running international payments through traditional banks and consistently seeing gaps between what you send and what your suppliers confirm receiving the correspondent chain is likely the cause.

At Linka, we work with CFOs, treasurers, and operations teams across Latin America to build payment flows that are cost-visible, fast, and reconciliation-clean. We don't eliminate all costs but we make every cost visible before you commit.

Reach out to our team to review your current payment corridors and run a real cost comparison: linka.xyz

Follow us on LinkedIn and X for weekly insights on cross-border payments, stablecoin infrastructure, and treasury operations across Latin America.